SHOULD YOUR TOTAL TAX RATE (fed, state & local taxes)

BE DOUBLE THE TAX RATES OF BILLIONAIRES & EXXON?

THINK NOT? ... CLICK TO LEARN MORE & SEE THE FIX

This Essay is for students of the plan, who have an hour to spend. Not you? Start Here!

FUNDAMENTAL TAX REFORM: THE FAIR SHARE TAX

FairShareTaxes.org

It is past time to overhaul the way we pay for the services that our governments provide for us in the United States. The current system of multiple taxes, when considered as a whole, is grossly unfair. It is weakening our economy and underfunding our governments. It has repeatedly led to financial meltdowns by distorting market forces and encouraging the formation of financial bubbles. It is underfunding current government obligations creating a large national debt for future generations. It is so complex that each year billions of dollars are spent to administer, comply with, and evade it. This essay will show that adding a direct tax on each household's accumulated wealth (net worth) should be the cornerstone of any attempt to fix our tax system.

Few would dispute that under an equitable tax system, the contribution we each make toward funding the services that our governments provide for us should be roughly commensurate with the extent to which we profited from the services governments provide, that is, our financial means. A household’s financial means is largely determined by its wealth - its net worth - probably to a greater extent than its income. Who is better off: A family with a million dollars in the bank and an annual income of $30,000 – OR - a family with twice the annual income, $60,000, but $100,000 in debt? Yet, in the United States, accumulated wealth (net worth) is all but ignored in the determining the size of our tax bills.

As the country emerges from its latest financial crisis, it will need to increase revenues to pay for the various financial bailouts; our two wars; and investment in the long-neglected and interrelated priorities of education, accessible health care for all, medical research, energy independence, environmental protection, economic infrastructure, financial industry regulation, domestic security, and international aid. The private sector has no incentive to fund these priorities because the return (profit) on such investments takes many, many years to be realized and is spread diffusely throughout society. Therefore, these priorities require funding from government, that is from all taxpayers.

Even with the elimination of wasteful government expenditures, failure to increase government revenues would underfund these priorities, leave the United States a debtor nation, further enrich competing, often hostile nations that are servicing our debt, increase inflation, reduce credit available to the private sector, and burden future generations with our debt. Our nation would decline further as a force to advance human rights and foster prosperity here and throughout the world. In short, billions of people would suffer.

However, we need to take care in how we go about increasing taxes. Increasing taxes on the middle class would likely decrease consumption and so trigger a slide back into recession. Continuing current tax policy that favors investment income and gains over income from work and savings and promotes wealth concentration in the top few percent will result in a continuing string of investment bubbles and the recessions they cause. As demonstrated in the remainder of this essay, increasing the taxes of the wealthy, while decreasing taxes of the working-poor and middle-class, would move us toward and equitable tax system, improve the economy and strengthen the nation.

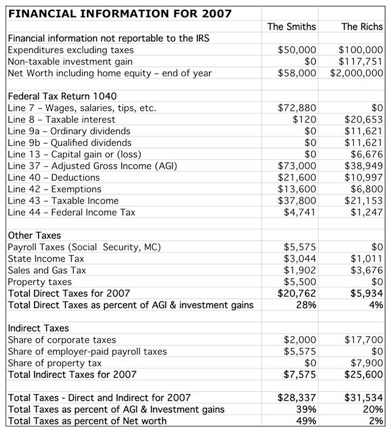

Consider the financial circumstances and tax liabilities of two hypothetical families. Their most important financial data, including figures from their 1040’s, are in this chart.

Mr. and Mrs. Rich are each 45 years old, have no children, and live in the same Long Island town as the Smiths. After college, Ms. Rich worked at her father’s business for 20 years and then retired. Five years ago she inherited $800,000 from her parents. Mr. Rich stopped working when he married three years ago and brought no assets or debts to the marriage. They lease a seaside condominium for $2,500 per month. In 2007, the Richs had a combined income and investment gain of $156,700. They spent $100,000, excluding taxes. Their net worth at the end of 2007 was $2,000,000, including $800,000 in Mrs. Rich’s 401k accounts. Their savings and investments, mostly in stock mutual funds, yielded an average of 8% in 2007.

Our two hypothetical families demonstrate that under our patchwork of federal, state, and municipal tax systems, a middle-class family with both spouses working hard to make ends meet can pay a total tax rate of 39% per dollar earned through work. That rate is about two times greater than the millionaires’ tax rate per dollar of investment income and gain. The middle-class family pays 49% of their net worth in taxes, while the millionaires pay less than 2% of their net worth. The examples were constructed without contriving any unusual circumstances or applying any tax shelters or “loopholes.” (For details of the tax calculations, see this spreadsheet.)

How the Richs legally avoid paying their fair share in taxes. Many of the Richs’ tax advantages over the Smiths are due to their living off of investments rather than wages. Although the Richs’ investments yielded about $157,000 over the year, 75% of it was in Mrs. Rich’s tax-deferred retirement account and/or in the form of unrealized capital gains. These investment gains are not reportable to any tax authority and are not taxed. The Richs can redeem the money they spend from their investments while keeping their taxable income low by selectively selling those assets that have gained the least and offsetting some of those taxable gains with paper "investment losses" from prior years. On the other hand, the Smith’s income consists of only wages and a bit of interest on their savings, both of which are fully subject to federal and state income taxes. Since making the down payment on their home, they have not re-accumulated enough money to open a tax-deferred retirement account.

The example of the Richs shows how easily the wealthy can keep their taxable income low in order to minimize the taxes they owe. With two million dollars in assets, their adjusted gross income was only about $39,000, even though they made $157,000 in investment gains in 2007. They were able to spend $100,000 and increase their assets by $57,000 in the same year. Obviously, the recently proposed and defeated federal income tax increase on those earning over $250,000 would not increase their taxes at all. This shows we need much more comprehensive tax reform.

For the Richs’ federal income taxes, two classes of investment income - qualified dividends and long-term capital gains - represent 90% of their reportable income and were taxed at 9% (federal and state combined), about half the rate they would have paid had they earned the money in wages or interest. Nationally, three-quarters of these tax-favored investment gains go to the top 1% income-earners. The Smiths paid the full tax rates on all of their income, and have a combined federal income, federal payroll, and state income marginal tax rate of 33% on every extra dollar they earn in wages or savings account interest.

The federal income tax accounts for only 30% of all taxes collected in this country. Most of the other 70% further shift the responsibility for paying for government services from the wealthy to the working-poor and middle-class.

The so-called payroll tax is distinct from the income tax and is used exclusively to fund Social Security and Medicare. Since the Richs have no wages or business, they pay no payroll tax. Because they each worked and paid payroll taxes for ten or more years, they will be eligible for Social Security and Medicare benefits. Almost all of the Smiths’ income is in wages, and so is subject to payroll taxes. Like two-thirds of American families, they pay more in payroll taxes than they pay in federal income taxes. Only the first roughly $100,000 of each worker’s earnings is taxed to fund Social Security, so this is in effect a regressive tax (a tax imposed in such a manner that the tax rate decreases as the amount subject to taxation increases).

The Richs do pay more in sales taxes than do the Smiths, because they buy more non-food and other non-exempt items. The Smiths pay more in gas tax because they each commute to work by car and have older, less energy-efficient cars. Compared to the wealthy, the poor and the middle class generally pay a much greater percentage of both their income and their wealth (net worth) in sales and excise taxes.

The Richs do not own a home, so they pay no real estate property taxes. None of the their property, their net worth of $2,000,000, is considered in determining any of their taxes. The Smiths’ property tax is based on the appraised value of their home, $250,000, even though they have only $34,000 of equity in the home. As a result, they pay property taxes on more than four times their net worth. Even if the Richs bought their rented condominium outright with $400,000 of their fortune, only one-fifth of their net worth would be taxed through the property tax, and their total direct taxes would still have been about $8000 less than the Smith’s total taxes.

Indirect Taxes. There are also hidden indirect taxes that we pay. Although we do not write the check to the government, the taxes are really paid by us. The main indirect taxes we pay are corporate taxes, the employer's part of the payroll tax, and, for renters, a portion of the property taxes paid by their landlords. The following calculations are based on conclusions that are widely accepted by economists who have studied the matter.

Federal and state corporate taxes for 2007 were about $440 billion dollars on $1730 billion profits. Corporations are aggregates of investor owners and workers (capital and labor). Economists agree that about half of corporate taxes fall on investors in reduced dividends and share prices, and the other half falls on labor in reduced wages and increased prices. Thus of the $440 billion in corporate taxes, $220 billion comes out of the pockets of investors and the remaining half out of the pockets of workers (say $110 billion) and consumers (say $110 billion).

Corporations pay out about 10% of their after-tax profits to shareholders in dividends, which totaled $156 billion in 2007. Without a corporate tax they would have been expected to pay out $22 billion or 14% (156+22/156=1.14) higher dividends. Therefore, the value of a 14% loss in dividends (in both their taxable and nontaxable accounts) has been added to the indirect tax bill of the Richs. The remaining 90% of the $220 billion in corporate taxes represents reduced cash in corporate coffers. This $198 billion reduces the the 2007 US total stock market value by 1% (total market capitalization $16500 billion; (16500+198)/16500=1.01). Therefore, the the Rich's indirect taxes also includes 1% of their stock holdings.

If corporate taxes reduce wages by total $110 billion, this amounts to about 2% in reduced wages (total US wages $5842 billion; (5842+110)/5842=1.02), so the Smith's indirect tax bill includes a 2% loss in wages. Finally, if corporate taxes increase prices of all goods by $110 billion, this amounts to a 1% increase in prices (total US consumption $9240 billion (9240+110)/9240=1.01), so both families' indirect tax bill includes 1% of their expenditures.

Nearly all economists that have considered the matter believe that about 100% of the employer-paid portion of payroll taxes (funding Social Security and Medicare), are in fact paid by the worker. Employers consider the total compensation to workers, including employer-paid payroll taxes, in negotiating wages with workers. Therefore, without this tax, employers would very likely pay an equivalent amount to the employee in wages.

The landlord's property tax expenses on rental properties are generally passed along to renters in increased rent. However, the landlord deducts this expense from his rental profits in determining his income taxes. Assuming a marginal income tax rate (combined federal and state) of 30%, leaves 70% of property taxes to be passed along to renters in increased rent. For the calculations here, the following assumptions were used: A typical 17:1 property value to annual rent ratio, a 2.2% property tax rate, and that 70% transfer of property tax burden to the renters. This yields a $7900 indirect property tax for the Richs.

The very wealthy and the working poor. The Richs are modestly wealthy, with a net worth in the top 5% of United States households. The tax breaks they enjoy are even more generous for the extremely wealthy. Three-quarters of investment gains, which are taxed at maximum rates that are less half the maximum rates paid by wage-earners, go to the top 1% income-earners. Fifty percent go to the top 0.1%. Warren Buffett, then the third richest man in the world, disclosed his income and payroll taxes for 2006 when he stated, "But I think that people at the high end -- people like myself -- should be paying a lot more in taxes." He reported a federal tax bill of about $8.1 million or 17.7% of his "income." Adding in state income and other personal taxes, his tax rates were about 25% of his federally-defined income.

However, Mr. Buffett's investment gain for the year was $8.1 billion, about 180 times his federally-defined "income." Put another way, over 99% of that investment gain was taxed at a rate of 0%. The very wealthy can live in luxury on a tiny fraction of their accumulated wealth. Therefore, they never need to cash in their capital gains (and can even borrow against them) to allow them to grow tax-free year after year, which adds substantially to their returns. Further, the tax liability for capital gains resets to zero when a wealthy person dies and passes his wealth to his heirs.

Middle class savers do not get this break on their savings accounts. They need to pay taxes on their interest every year, which cuts into their compounded interest substantially[e.g. A $1 million investment earning 8% each year for 30 years grows to $6.8 million after the application of a 25% capital gains tax only in the 30th year. It would have grown $1.1 million less if the 25% tax on capital gains was applied every year.]

Yet, a fair assessment that includes all Mr. Buffett's investment gains as a sort of income in the calculation of his tax rate should also include the corporate taxes he in effect "paid." His total taxes, including those corporate taxes amounted to $794 million. That is, about 75 times the personal direct taxes he paid. With those and other indirect taxes included, his total tax rate was 11% of his income and investment gain and 1.8% of his year-end net worth. The same calculation was extended over a 10-year period 2000-2010 and found his tax rate including corporate taxes to total 10% of his income and investment gains over the period.

In comparison, our middle-class Smiths paid over $28,000 in total direct and indirect taxes. That is 39% (vs. Buffett's 11%) of their income and (non-existent) nontaxable investment gain. It is also 49% (vs. Buffett's 1.8%) of their net worth. By these measures, the middle-class Smith's tax rates are (respectively) 2.5-fold and 27-fold higher than the rates paid by Mr. Buffett.

[Mr. Buffett's portion of corporate taxes is calculated as follows: Berkshire Hathaway federal and state corporate income taxes from its 2007 annual report multiplied by his personal share of Berkshire Hathaway ownership multiplied by estimates from the academic literature on the portion of corporate taxes ultimately borne by capital (rather than labor and consumers) $4900 million x .32 x .5 = $784 million. For details see this spreadsheet.]

The Internal Revenue Service reports that in 2007 the average income of the top 400 earners was $345 million, and they paid an effective federal income tax rate of 16.6%. The middle-class Smiths paid a federal income tax rate of 6.5%, demonstrating that the federal income tax is progressive. If you add in payroll taxes though, the Smiths pay a total federal tax rate of 14.1% while the top 500 still have a federal tax rate of about 17%. Only wages, not investment income, are subject to the payroll tax. Adding the Smiths state and local direct taxes and their total taxes amount to 28% of their income. Add their indirect taxes and their tax rate becomes 39% of income, compared to the 11% figure calculated the very same way for Mr. Buffett.

We often hear that half of American households pay "no taxes." This sound-bite is simply wrong. About half of households pay no federal income taxes, but federal income taxes account for less than 25% of all taxes collected in this country. Most of households that pay no federal income taxes are households made up of the elderly and disabled living on Social Security, the unemployed, students with part-time work, and large families earning very low wages. (However, thanks to tax breaks for the wealthy, those paying no federal income taxes also included over 10,000 taxpayers with a "federal annual gross income" of over $200,000.) There is probably no non-institutionalized adult in the USA who truly pays no taxes - no Social Security taxes, no sales taxes, no property taxes, no gas taxes.

Considering all forms of taxation, even a single worker making minimum wage pays over $5000 in total (direct and indirect) taxes annually. That is 37% of her annual wages of $14,500 and could easily be 10 times (1000% of) her net worth. Her taxes include over $1800 in direct federal income and payroll taxes, $800 in other direct taxes and $2800 in indirect taxes. She would not qualify for the earned income tax credit or for food stamps. (Two-thirds of all "entitlements" go to the middle-class and the wealthy, to households well above the poverty-line.) A typical widow living off of Social Security benefits of $12,900 (after Medicare premiums are taken out) pays about $2550 or 20% of that income in taxes. This assumes she pays typical property ($2030), sales ($400), and gas taxes ($120) for a retiree. In some parts of the country, property taxes on typical homes are two-fold higher, bringing such a widow's total tax rate to about 35% of her Social Security income.

The current tax system is unfair and distorts incentives. Taken as a whole, the tax system in the United States is very regressive despite the fact that the federal income tax is more or less progressive. The four taxpayers discussed here demonstrate this nicely. To recapitulate, the total taxes paid as a percent of all income and investment gain are 37% for the minimum-wage worker, 39% for a middle-class working family, 20% for a investor-class millionaire couple, and 11% for a billionaire investor. As a percent of their net worth, total taxes are about 600% for the minimum-wage worker, 49% for the middle class working family, and under 2% for the millionaire and billionaire investors.

In the United States the wealthiest 1% now hold about 40% of the wealth, while the bottom 40% hold about 1% of that wealth. Thirty years ago the top 1% owned 22% of the nation's wealth but the figure started increasing toward its current level of 40%, shortly after President Reagan started cutting taxes on wealthy. The tax cuts on wealthy investors were extended in 1997 and 2003, when investment income was assigned special reduced tax rates, about one-half the rates paid by workers on their wages. The benefits of those tax cuts stayed with the wealthy; they have not “trickled down” to the poor and middle class as supply-side theorists predicted. The wealthy use their money to influence lawmakers to further protect their wealth from taxation. The nation is becoming an ossified, almost feudal society in which the concentration of wealth leads to a concentration of power, which leads to a further concentration of wealth, and so on in a vicious cycle. This is a threat to our democracy. When polled, Americans believe that the most talented and hard-working should get ahead - within reason. On average, they feel that it would be fair for the wealthiest 20% to hold 33% of the nation's wealth. They wealthiest 20% actually hold 85% of the nation's wealth.

[Does our tax system really account for the wealth concentration over the last 30 years in which the top 2% has gone from holding 28% to 48% of the nation's wealth? A simulation with two groups - the "Top 2%" and the "Other 98%" - helps answer this question. The simulation starts with the Top 2% holding 28% of the nation's wealth, as they did in 1980. Each of the Top 2% has a net worth of $2 million, like the Rich's of this essay. Suppose they don't work, earn less than average stock market gains for the period, 8% per year, and spend $100,000 per year. Their direct total tax rate is higher than Rich's, 10%. The Other 98% are much like the Smith's. They start with a net worth of $60,000, mostly in home equity. Their net worth appreciates 3% per year (higher than typical gains in house values and savings accounts, where workers hold most of their wealth). They work with wages of $70,000 per year and spend half of what the Top 2% spend, $50,000 per year. Their direct total tax rate is the same as that calculated for the Smiths, 28%. Run that simulation over 30 years and the top 2% go from owning 28% to 47% of the nation's wealth. Each in the Top 2% has had their net worth more than triple. That's almost exactly what's happened over the last 30 years. If instead the total tax rate of that Top 2% was the same rate as that of wage-earning workers for those 30 years, that Top 2%'s share of nation's wealth would have increased only slightly from 28% to 31%. The lesson is clear. If you have great deal of money, you do not need to work, you can spend more than the average worker would ever dream of spending, and still get much wealthier ... but only providing you are taxed at rates about one-third of what wage-earning worker pay.]

Whenever it is suggested that the wealthy pay their fair share of taxes, the cry goes up: "But the top 5% already pays 60% of taxes." This is misleading. Firstly, the top 5% own 55% of the wealth in this country. It seems that they are under-taxed if they pay only 60% of the taxes while 14% of the nation lives in poverty. However, secondly, the sound-bite is wrong. The correct statistic is: The top 5% of households in terms of federal adjusted gross income pay 60% of the federal income tax. That is, the sound-bite refers only to federal income tax on federally taxable income. Federal income tax accounts for only about 25% of taxes collected from individuals in the United States. Our other taxes, like payroll taxes, sales taxes, excise taxes, and property taxes, shift the total tax burden from the wealthy investing class to the working middle-class. It is more nearly accurate to say the top 5%, who hold 55% of the nation's wealth, pay only about 35% of all taxes in the United States.

Thirdly, the argument that "because the very wealthy pay most of federal income taxes means they are paying enough" is simply not a valid argument. Under that logic (in a 20-person economy), it would be fair to charge each of the 19 bank tellers a 100% tax on their $15,000 yearly incomes and charge the bank executive a 4% tax on his $10,000,000 salary ... because, after all, the top 5% (the bank executive) would be paying about 60% of all taxes. In addition, the very wealthy, to a much greater extent than the middle class and poor, can take advantage nontaxable compensation, adjustments to taxable income, more tax savings for each deduction, reduced tax-rates on some investment gains, no tax on other investment gains (such as unrealized capital gains), and tax-exempt accounts to avoid taxation on their actual income. This and the fact that accumulated wealth is ignored in the determination of taxes results in the wealthy shouldering far less than their fair share.

All taxes create incentives that distort the economy. The higher the tax on an activity is, the more expensive that activity is, and so the more that activity is discouraged. The Smiths paid about 18% in federal income tax, state income tax, and payroll taxes for every dollar they earned through work. The Richs paid 1.2%, about 15-fold less, in federal and state income taxes on every dollar of investment income and gain. Considering total taxes, the middle-class family paid a tax rate per dollar earned though work that was two times greater than the millionaires’ tax rate per dollar of investment income or gain. This is not only inequitable, but also has the effect of discouraging work relative to the activity of investing. Although investment is important to the operation of our economy, it is hardly 2-fold (or 15-fold) more important than work.

None other than Abraham Lincoln said, “Labor is prior to and independent of capital. Capital is only the fruit of labor, and could never have existed if labor had not first existed. Labor is the superior of capital, and deserves much the higher consideration.”

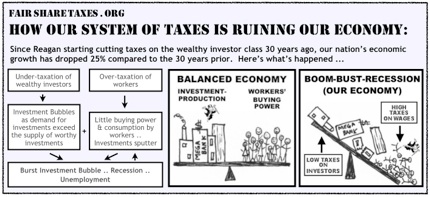

Reduced tax rates on investments are touted as stimulating the economy by encouraging investment. Viewed another way, giving investment gains preferred tax treatment distorts the investment market. As discussed further below, it likely increases the demand for investment vehicles to the point it exceeds the supply of good investments, and so contributes to the formation of investment “bubbles,” which inevitably “burst” to throw our economy into turmoil.

A wealth tax makes the tax system fairer. When all property, total net worth, is considered as the basis for total taxes paid, the Smiths’ tax rate is much much higher than the Rich’s. The middle-class Smiths’ tax rate per dollar of net worth is 30-fold greater than the millionaire Richs’. The fact that the Smiths’ small extra income in savings interest ($120) is taxed ($27) while the Richs’ $2 million fortune is not considered in determining their ability to pay taxes is as astonishing as it is indefensible. Wealth as well as income must be taxed to make taxes proportionate to ability to pay.

Taxing accumulated wealth and a progressive overall tax system is fair in another respect. The wealthy, to a disproportionately greater extent than the working-poor and middle-class, have amassed their wealth by exploiting the “economic infrastructure” provided by governments (i.e. all tax payers). For instance, compared to the middle class, those who have become very wealthy through commerce and investment have generally benefited more from: physical infrastructure (e.g. highways for trucking); inexpensive fuel (subsidies, the military); twelve years of public education plus subsidized higher education (of their employees or employees of companies they invest in); Social Security and Medicare (which maintain a non-destitute retired class able to keep consuming); the Earned Income Tax Credit (maintains consumption but businesses can pay less than a living wage); subsidized medical care for those injured by pollution, harmful products, and employment; environmental cleanups; government-funded basic research; the internet(!); domestic order (system of laws, police forces); a judiciary (to adjudicate commercial disputes); economic stability (fiscal and monetary policy); business regulation; corporate subsidies; financial industry bailouts (!!); and so on.

In addition to favored tax rates for the investor-class, many other tax breaks go to the wealthiest. For instance the top 15% income earners get 55% of the tax breaks for employee provided retirement benefits. Ten percent of all "entitlements" go to the wealthy, to the top 20% of households. Such services are provided by governments and paid for to a great extent by working-poor and middle-class taxpayers. They should not be paying greater tax rates than the wealthy since they have profited from these government services much less than the wealthy have.

Consider, for instance, what sort of profit a wealthy investor in a large corporation would be able to make if that corporation's workforce did not receive twelve years of public education, paid for almost entirely by the property taxes on the middle-class. Do this thought-experiment: What would happen if that public education (starting with reading, writing, and arithmetic skills) was suddenly deleted from the brains of nation's workforce. Next remove the roadways and the other government benefits listed above. A minimum wage worker would continue to have a daily struggle to eke out an existence, but a millionaire would have their millions wiped out almost overnight. This thought experiment demonstrates who has profited most from government services. The millionaire's fortune is entirely dependent on government services, but he is now paying for those services with total tax rates (as a percent of net-worth) that are about 300-fold less than those paid by minimum-wage workers.

The real estate property tax, the only significant levy approximating a wealth tax in the United States, is an irrational, often unfair, and generally regressive way of taxing wealth. It is a vestige of an agrarian time when almost all of a household’s wealth was in its real estate holdings. As shown above in the example of our hypothetical families, the real estate tax is levied on many times the net worth of most families, but a generally a small fraction of the net worth of the very wealthy. Further, taxing the full market value of a home, rather than a family’s equity in it, places a disproportionate tax burden on young families attempting to gain a financial foothold. Farmers pay a large property tax on their land (their property on which they make money), while investors, pay no tax on their net-worth (their property on which they make money). Finally, the property tax does not change when there is a sudden change in a family’s ability to pay. Should both the Smiths of this essay become unemployed, their total annual tax bill would still be about $7500, 80% of which is the property tax on their home.

The estate tax, a tax of up to 55% on very large estates, is a one-time onerous tax bill on the very wealthy. The upshot is that lawmakers have written laws to allow the wealthy set up trusts and other legal maneuvers avoid 80-90% of this tax. Thus the estate tax accounts for only about 1% of federal revenues.

Taxing unrealized capital gains as income could be an option to make the taxes of the investing class more proportionate to their means. However, such a tax would be impractical, as it would result in massive unpredictable swings in government revenue each year.

A tax on accumulated wealth, that is net worth, beyond a large deductible would allow for the elimination of the estate tax. As indicated above the estate tax is largely evaded. Further, we often hear complaints that a large estate tax disrupts the inheritance of family businesses. A net-worth tax would mitigate this by collecting taxes on accumulated wealth in manageable bits over a lifetime rather than a one-time payment of up to 55% at the time of death.

A net-worth tax would also allow for the elimination of capital gains taxes as well as estate taxes. For instance, a 1% tax on net-worth amounts to 20% tax on a presumed average annual return of 5% on investments. Currently capital gains taxes have three problems: 1) They discourage investors from moving money to the best investments in order to avoid taxable realized gains 2) Unrealized gains go untaxed, giving investors an advantage over interest-bearing saver since their returns can grow tax free, year after year. 3) They create a book-keeping burden, are difficult to tax authorities to check, and so are often evaded. Taxing investment gains indirectly through a net-worth tax mitigates each of these problems.

A household’s financial means is determined by its wealth, probably to a greater extent than its income. Therefore, in order to make taxes commensurate with ability to pay and proportionate to the extra benefits the wealthy have derived from the government services, a household’s wealth - as well as its income - must be taxed. Net worth is the universally accepted best measure of a household’s wealth and so is the obvious choice to be the basis from which a wealth tax is calculated. Several developed nations, including Norway, Switzerland, and the Netherlands, all with very strong economies, have recognized all this is true and instituted a tax on net-worth.

Our economy is far from ideal. Ideally an economy should allow a meaningful livelihood for all those able to work. It should allow for a basic decent standard of living for all, including those truly unable to work. It should offer some basic fairness, meaning equal opportunity for each individual and that each household’s standard of living is roughly commensurate with its member’s talents and efforts. It should promote activity that reduces suffering throughout the world. Finally, the economy should make provisions to assure these goals - full employment, a decent standard of living, basic fairness, and reduced suffering - for future generations.

For an economy to promote each of the above goals, it seems that its four components must be at the correct absolute levels and correct levels relative to each other. Those four components are production, consumption, private investment, and public investment.

Production is making products or providing services. In essence, it is work. Consumption is the spending to acquire those products and services. In private investment, money not needed for immediate consumption is put aside in savings, generally bundled by banks and corporations with money other individuals, and used to fund larger profit-making endeavors. In private investment, the payoff is generally expected to be prompt and go primarily to the savers and investors in the banks and corporations that did the bundling. These first three components of the economy are generally carried out by individuals or businesses (financial aggregates of individuals).

Examples of public investment are road building, education of children, basic science research, national defense and insuring that the disabled and elderly do not live in poverty. As in private investment, there is the bundling of money from many individuals for large endeavors. However, in public investment, the payoff is diffuse, going to individuals and businesses throughout society, and/or the payoff is expected far off in the future. Because private investors cannot capture the profit from such endeavors, they are unwilling to make these investments. Therefore, governments (and to a much smaller extent non-profit organizations) carry out public investment. We have empowered our governments to fund such endeavors by requiring payments from their citizens in the form of taxes.

Our current tax system places levies on the first three components of the economy: taxes on work-production (income and corporate taxes), taxes on spending-consumption (sales and excise taxes), and taxes on private investment (income and corporate taxes). The other major tax, the real estate property tax, is generally a tax on home ownership, a hybrid of consumption and investment. Taxes tend to discourage an activity by making it more expensive, so the rates and relative rates of taxation significantly affect the extent to which individuals and businesses engage in work, spending, and private investment. The amount of tax revenue collected obviously determines the extent to which the fourth component, public investment, can be engaged in.

There are two major problems with our economy that keep it from being the ideal economy described above.

The first major problem is that we are not making sufficient public investments to promote an efficient economy now or assure a strong economy for the future. For example, in many schools children are not being provided with the basic skills that they will need to perform the jobs of the future. Because the new global economy and cheap unskilled labor abroad, undereducated and unskilled people here cannot find work and become productive members of our society. There are scores of other examples, including: We are not funding the basic research that could develop into the new economies of the next decades. Every day millions of man-hours of productivity are lost because of our neglected transportation systems.

The second major problem with our economy is that we have frequent recessions. The following shows how our current tax policy causes or exacerbates recessions. Insufficient private investment hurts an economy but so does excessive private investment. The last two recessions were triggered by an excessive investment in new technology stocks (dot-com equity bust of 2001) and housing securities (housing bust of 2008). A bubble is, in essence, excessive demand for investment that outstrips the supply of worthy investments, artificially driving up investment prices to unsustainable levels. Market forces overwhelm any attempt to rein in "irrational exuberance" through regulation. The number of worthy private investments is determined by the the economy's capacity for production and consumption. Wealth that is not spent is saved, meaning that increasing investment dollars must reduce consumption. The concentration of wealth in richest few means that even more dollars are diverted from consumption to investment, since the very wealthy can spend only so much. Governments then step in bolster economic growth with artificially low interest rates, which induces high debt for the poor and middle class. At some point there is a realization that without sufficient consumption, there will be no or little return on investment, and the artificially high investment prices drop precipitously. The bubble bursts and a recession ensues as investment, consumption and production drive each other downward in a vicious cycle.

What happens in a recession? Jobs are lost, salaries are cut, and retirement savings are wiped out. Houses are foreclosed on, health insurance is dropped, and young adults loose their chance for higher education, damaging future economic growth. Some families who worked hard to get a leg up never recover. Tax revenues drop. Lawmakers, not recognizing that a recession (and perhaps a recession alone) justifies increased deficit spending, slash education, research, and infrastructure spending. This sabotages any economic recovery and hobbles economic growth for the next generation. In short, millions of hard-working Americans suffer. They see the wealth disparity in our country more clearly and become angry. This leads to political instability, damaging the economy further. The size of the United States economy means that the suffering caused by our mismanaged economy spreads worldwide, doubling back to damage our economy further.

Yes, our economy is far form ideal. In a study of the 18 developed economies (The US, Canada, European countries, Australia, New Zealand, Japan, and South Korea), the United States was dead last in economic equality, overall poverty rates, and childhood poverty rates. We were 5th last (of the 18 countries) in senior poverty and health-care quality. (link) About 3% of men, women, and children in the United States go hungry at some time each year. Social mobility in the United States is a myth. Among boys raised in the bottom one-fifth here, 42% stay there as adults. That number for Denmark and Britain, for instance, is 25% and 30%. (link) Forty-one percent now say there is not much opportunity in America, up from 17% in 1998.

The Historical Evidence. It is probably not coincidental that the two most recent investment bubbles began here in the United States, the industrialized country with the greatest wealth disparity and that each occurred (2001, 2008) a few years after investments were given even more favored tax treatment (1997, 2001, 2003), increasing wealth disparity further. The favored tax treatment of home ownership likely also contributed to the recent housing bubble.

Nor is it coincidental that the Great Depression was triggered by the US stock market crash in 1929 just after the last time our wealth disparity reached the levels reached in 2000. That crash followed the real estate and stock market bubbles - of the Roaring Twenties - which was caused the massive Republican tax cuts from 73% to 25% for the wealthiest. Then, from the 1930s to the 1980s, the top marginal tax rates for the wealthy increased to about 70%. During that period the economy grew steadily, we went 50 years without a crash or major bank failure, and worker’s wages increased enough to produce opportunities for the working-poor and a large, prosperous middle class.

Economists at the International Monetary Fund published a study in 2011 that confirms that wealth disparity is associated with shorter periods of steady economic growth. Countries that have a narrower gap between rich and poor enjoy longer economic expansions, that is, fewer recessions. According to economist Jonathan D. Ostry of the IMF, income trends in the U.S. mean that future U.S. expansions could last just one-third as long as in the late 1960s, before the income and wealth divides began widening.

It is often argued that increased taxes on the wealthy would damage the economy because the wealthy drive the economy and create jobs. Let us look at the last 60 years. From 1951 to 1986, America’s highest marginal federal income tax rate ranged between 50 percent and 92 percent, and the nation’s average annual growth in gross domestic product was 3.6%. However, during the next twenty-two years, 1987 to 2009, after the top tax rate was cut and while it was 35 to 39%, the economy grew at an average of just 2.7%, only three-quarters of the previous average rate of growth. (This drop in GDP since we started cutting taxes on the wealthy may be even worse. Some economists believe that starting 30 years ago, a change in the method of calculating real GDP started artificially inflating the number.) The average unemployment rate was the same, 5.7%, during each period. No, favored tax rates for the wealthy does not “create jobs.”

Right now, the top 5% now hold 70% of the nation's wealth, up from 35% 30 years ago. Corporations are now holding a record $1,100 billion in uninvested cash. If giving more money to very wealthy investors and cash-bloated corporations creates jobs, where are those jobs? As of this writing, the unemployment rate is over 8%. No, the tax breaks for the wealthy and corporations are real failed stimulus package, and have cost the Treasury 10-fold more than the much-maligned stimulus package of 2009.

What about the incomes of Americans in the two 30-year periods before and since tax cuts for the wealthy started under Reagan? In the 30 years before Reagan, the average inflation-adjusted income for the typical American, the bottom 90%, increased $13,000 or 75%. In the 30 years after Reagan started cutting taxes on the wealthy, it went up only $600 or 2%. During that same post-Reagan period, the average income of the top 1% tripled (increased about 200%) or about $1,000,000. There was no “trickle down.”

Excessive investment caused by our investment's favored tax treatment does not only hurt workers by triggering recessions. It also hurts investors directly. In the 18 years before the special tax rates for investment gains went into effect in 1998, the inflation-adjusted annualized return of the S&P 500 companies was 8.8%, close to its historical average. In the 13 years since those favored tax rates for the wealthy went into effect, the inflation-adjusted annualized return of the S&P 500 companies (1998 to mid-2011) dropped to 1.6%. That is, the historic return on stocks went into free-fall, down to one-fifth of what it previously was. This hurt the wealthy, but it also hurt the middle class, which has much of its retirement savings in the stock market.

A reformed tax system with a net-worth tax benefits the economy. Against this background, what would the effect of a fairer tax system be? Let us say the system includes a tax on household net worth exceeding several hundred thousand dollars, a reduced tax on wage income, the elimination of generally regressive employee payroll, sales and property taxes, and the elimination of favored tax treatment of investment income and home ownership. Investment income and gains would no longer be untaxed or taxed at a lower rate than work.

The result would be: Taxes on the wealthy few would increase, and taxes on the vast middle class would decrease. Most importantly, private investment and consumption would come back into balance (remember the see-saw). There would be sustainable growth of both, with fewer and milder investment bubbles and recession.

The end of the market-distorting favored tax treatment of the wealthy and reduced taxes on the working poor and middle class would partly reverse the trend that has over the past four decades concentrated the nation’s wealth and power in fewer and fewer households. It would allow a decent standard of living for all and make each household's standard of living more commensurate with its member's talents and efforts. The current concentration of wealth in the United States is much higher than that thought to be ideal for economic growth.

The middle class tends to spend most of any additional after-tax income, so reducing their total taxes and eliminating the sales tax would increase spending (consumption). The very wealthy are a small fraction of the population and tend to save and invest rather than spend any additional after-tax income and wealth, so Increasing their taxes as proposed would have little effect on overall consumption. Consumer consumption accounts for about two-thirds of our economy. Increased baseline levels of production and consumption make the economy more recession-resistant.

Reduced taxation on work income would promote work (production). Overtaxation of working-poor and middle-class workers relative to wealthy investors impedes economic mobility, which is now lower in the United States than much of the developed world. When a nation’s institutions, including its system of taxes, prevent the poor from profiting from their work, the average person can not share in the growth of the economy. This saps the motivation of workers, which destroys economic growth. Over two hundred years ago Adam Smith, the father of capitalism, wrote about this in The Wealth of Nations. In his book Why Nation’s Fail. MIT economics professor Daron Acemoglu shows how institutional impediments to economic mobility (e.g. our regressive system of taxes) leads to failed economies and failed nations. On reviewing the evidence a New York Times economics reporter writes, “It’s hard to read these sections without thinking about the present-day United States, where economic inequality has grown substantially over the past few decades. Is the 1 percent emerging as the wealth-stripping, poverty-inducing elite?”

[A Value Added Tax (VAT) or other new taxes on consumption would exacerbate the current problems with our economy. A VAT would concentrate wealth further, taxing investment income and gains not at all, and discouraging consumption. For instance, under the proposed "Fair Tax," proposed by some Republican members of Congress, Warren Buffett's federal tax bill (including his share of corporate taxes) would drop from about 11% to 0.04% of his income and investment gains, a 250-fold drop. This would worsen the favored tax treatment for private investments and wealth disparity. Any attempt to end investment bubbles by regulation alone would be overwhelmed by these distorting market forces. The world would be thrown into a Depression that would make would make the Great Depression look like a party.]

Would the fairer tax system described above result in too little private investment? This is unlikely. A tax and the (likely associated) elimination of a capital gains taxes may encourage investors to move investments from unproductive investments to more production ones with better returns. Right now the tax system awards wealthy investors who forever hold on to an investment, since the gains are perpetually untaxed as long as they do. Further, the tax system can be designed to encourage the working-poor and middle-class to save and invest some of their newly increased after-tax income. Thus the "job doers" would also become "job creators." by investing in our economy. For example, tax free-accounts could be mandated for all adult employees except those opting out. The caps on these accounts could be adjusted to optimize the overall amount of private investment.

[Some will object to this as a socialistic governmental attempt to manipulate the economy. However, all tax policy alters the economy for better or worse. Further, those who argued for awarding investors with lower tax rates in 1997, 2001, and 2003 justified doing so by claiming that it would improve the economy. They were wrong, but they too were attempting to adjust market forces and alter the economy through government policy.]

Eliminating sales and property taxes would act as a buffer against recessions. Under the current tax system, if this essay’s hypothetical middle-class Smiths both lost their jobs, they still need to pay property and sales taxes, about $6500 annually. With those two regressive taxes eliminated they would have an extra $6500 in their pockets. It would reduce their monthly mortgage check (which includes payment into a property tax escrow account) by 30%. This would reduce their hardship substantially, might keep them out of foreclosure, and might sustain them until they find new jobs. It might allow them maintain their health insurance and thereby avoid the risking financial calamity from injury or illness. Further, they and families like them would not need to cut their consumption as much. This could help keep a slowing economy from spiraling into a deeper recession. Periods of increased unemployment would be mild and infrequent.

Reforming our tax system to put more money in the hands of the working-poor and middle-class would allow more young people to grow up in stable families and get advanced education and training. These and increased public investment in education in turn increase the likelihood that each person’s success is largely determined by their talent and hard work, rather than the financial means of his or her parents. Studies show that social mobility, as measured by income, is now lower in the United States than in Great Britain or Scandinavian countries. Promoting social mobility here and giving more Americans the opportunity to reach their full potential is certainly the most effective way to improve our economy, strengthen our nation, and make progress toward a better world. A World Bank economist, Branko Milanovic, has written: “Widespread education has become the secret to growth. And broadly accessible education is difficult to achieve unless a society has a relatively even income distribution.”

In summary, the proposed tax system would strengthen the economy. Production and consumption would flourish. That is employment, salaries, and standard of living would improve. Private investment demand would be contained and kept commensurate with production and consumption, reducing or eliminationg, investment bubbles and recessions. A vigorous economy would increase income and wealth, which would further increase tax revenue. Increased revenue and cuts in wasteful government spending (particularly somewhat reduced defense spending and reform of our health care system to make it more efficient) would reduce the national debt, reduce the fraction of taxes lost to paying interest on this the debt (about 7% in 2007), free up credit for the private sector, and allow increased government funding of our new, interrelated national priorities of: education, universal health care, basic research, energy independence, environmental protection, economic infrastructure, financial industry regulation, domestic security, and international aid. Each of these priorities is a public investment. Each of these public investments improve economic efficiency and help build a sounder, more vigorous economy for future generations. This increases tax revenue further and so on in a virtuous cycle.

A reformed tax system with a wealth tax benefits the poor, the middle class and the wealthy. Clearly, the middle class and working poor would do better under a reformed, fair tax system that reduces their taxes. The unemployed poor, who now may pay little in taxes, would do better from a better economy and increased government funding of economic infrastructure, particularly education. How? They could find employment and then pay their fair share in taxes. What about the wealthy? In a fair tax system, they pay more taxes, so surely they would be worse off. If one group wins, the other has to lose, right?

Wrong. Taxation is not a zero-sum game. To recapitulate, under a fair tax system, the average citizen works more spends more, saves and invests more, and can invest in education for themselves and their family. The government has more money to invest on economic infrastructure and “seed money” for research that would not be funded by the private sector (e.g. funding hi-risk basic energy research spawns new technology industries and averts climate-related human and economic catastrophe). The government borrows less, leaving more credit for the private sector. The economy is more stable with fewer and shallower recessions here and, given the growing interconnectedness of economies, abroad. These conditions would be a boon for the wealthy investor class. Returns on investment could increase several-fold to where they were before our Congress started giving investment income favored tax treatment. Over time, their investments are likely to increase much more than their taxes have. Thus, a fair system of taxes produces “a tide that raises all boats.”

Numerous academic studies have shown associations between economic inequality and poor health outcomes; such as higher infant mortality, worse general health, more psychiatric disease, more substance abuse, more homicides, and lower life expectancy. Economic inequality has also been associated with more teenage pregnancies, and low levels of trust and social cohesion. Among developed nations, these poor outcomes are generally not associated with the levels of economic growth, just levels of economic inequality. Interestingly, these poor outcomes associated with wealth disparity generally extend throughout a society. That is, they are not limited to the poorest segments of unequal societies, although they may be more pronounced among the poor. (link)

Currently 66% of polled Americans say their is a "strong" or "very strong" conflict between the rich and poor. This is up from 47% two years ago and much higher than perceived conflict between black and white or young and old (Pew Research Center). This sort of perceived conflict can lead to political instability, which can in turn harm economic growth and the well-being of all. A fair tax system would reduce this perception of class conflict and promote democracy. By reducing the concentration of wealth into very few families, it reduces their undue influence on our laws and government. Increased education opportunity for all increases the likelihood that future generations elect governments that are more likely to make further smart policy decisions.

Finally, under a fair system of taxes, the wealthy would benefit from the knowledge that they are giving back their fair share to society. Past generations of workers, taxpayers, and soldiers have made the prosperity of today’s wealthy possible. Today’s wealthy should be willing to contribute their fair share to making the prosperity of future generations possible. More and more of the wealthy are coming to this realization and in the words of a real estate millionaire: "Those of us who have the greatest ability to pay are not being asked to. I am not keen on being part of the freeloader class." Another millionaire said, ""It’s a sad state in this country when those of us who are so privileged fight for more rather than fight for those among us who have so little."

A proposal for reform of our tax system. The disproportionate influence of the wealthy on our tax laws, as they have been cobbled together over the years, is evident. Given our political system, changing our tax system to make each household’s taxes truly proportional to its financial means would require a Herculean effort, starting with campaign finance reform to limit the undue influence of the wealthy on our lawmakers. A federal net-worth tax might require Constitutional amendment. Nonetheless, attempting to design such a fair tax system on paper provides an ideal to begin to work toward. The following tax system is an example of a fair, effective, efficient method of funding government services:

In summary, at all levels of government:

1) regressive, inefficient, and hidden indirect taxes are eliminated;

2) the income tax is greatly simplified and its rates are reduced;

3) an annual net-worth (accumulated wealth) tax is substituted for current real estate, capital gains

and estate taxes; and

4) corporate taxes are ended (taxes on corporate profits are paid by the investors owning the

corporations).

-

•Eliminate payroll (Social Security, Medicare) taxes (regressive; instead these programs paid from general tax revenue)^

-

•Eliminate state income taxes in their current form (inefficient; instead states set & receive a surcharge on federal taxes)

-

•Eliminate sales and use taxes (regressive)

-

•Eliminate property taxes (very regressive; instead municipalities set & receive a surcharge on federal taxes)

-

•Eliminate capital gains taxes (currently most gains go untaxed; instead tax all gains indirectly through the Net-worth Tax)

-

•Eliminate estate taxes (instead collected in manageable bits through the Net-worth Tax)

-

•Eliminate corporate taxes (currently half are paid by labor; instead the human owners of corporations are taxed directly - see below)

-

•Eliminate tolls and lotteries (regressive and inefficient)

-

•Reform the Federal Income Tax, eliminating nearly all adjustments and deductions, with a uniform 20% tax rate on all income and compensation, excluding only the following, which are taxed at 3%:

-

•income below a realistic poverty line ($30,000 for a household of three (1-see notes below)

-

•large medical expenses and reasonable medical insurance benefits exceeding 6% of income(1), and

-

•limited contributions to tax-free accounts.

-

For a typical family of three, the effective federal tax rate would be: 3% on $20,000; 10% on $65,000; 15% on $140,000; 20% on $20,000,000+. All households pay a minimum $100 tax.

-

•Institute a new 2% annual Federal Net-worth Tax othe portion of households’ net-worths (that is, accumulated wealth) over about $800,000 (45 year-old couple with one child).(2) Only the wealthiest roughly 12% of households would be subject to any Net-worth Tax.

-

This tax is paid once a year tax on household net-worth as of December 31 and replaces current property, capital gains, and estate taxes.

-

The effective federal tax rate would range from 0.4% ($4000 tax) on a typical household’s net worth of

-

about $1 million up to 2% on net worths of $32 million or more.

-

•Small businesses and corporations with operations or sales within the US are required to calculate domestic US profits(3) using honest, standard accounting practices (without gimmicks, like accelerated depreciation). These domestic profits, excluding up to 30%(3), must be distributed annually to each business' owners and shareholders in proportion to their ownership stake. These distributions are taxed as ordinary income and paid by the owners or shareholders. Taxes on distributions to those who are both non-citizens and non-residents are withheld from the distributions at a standard 20% tax rate.

-

•Add a 6% War Tax surcharge on the Federal Income and Net-worth Taxes (e.g. increasing a $10,000 annual federal tax bill to $10,600; minimum $50 tax per household) whenever the nation is at war and two years after the war’s end (as a reminder of our obligation to our veterans).

-

•Fund state and municipal governments through a surcharge on each household’s combined Federal Income and Net-worth Tax (excluding any War Tax), with the surcharge rate set by each state and municipality. For efficiency's sake the federal government could collect the taxes and pass them directly (under law, free of any conditions) to states and municipalities. The average combined surcharge for funding state and local governments would total 50% of a household’s federal tax bill at first, but decline over the years.

-

•Retain excise taxes only on actions that society would like discourage since they have costs not reflected in their price. These include fossil-fuel-based energy, cigarette purchases, and failure to maintain Health Insurance Coverage (under the ACA, “Obamacare”). Except for the last they are charged at the time of purchase. For all poor and middle class households, this tax would be much more than offset by the reduction in their other taxes. For the poor, a small annual rebate could be given to cover the typical costs of excise taxes on items that are now largely not discretionary, like fossil-fuel-based energy.(4)

-

•Allow a single, unified, tax-free account for each adult with a modest age-dependent cap(5) up to to the lessor of 10% of income or $10,000 per spouse per year. It is set up automatically for wage earners at 5% of wages, up to $5000 per year, with options to increase contribution, decrease contribution, or opt-out entirely. The account can be tapped tax-free for activities that society would like to promote, education and saving for retirement. Contributions to, gains within, and distributions from the account are tax-free.

-

•Taxes apply to United States citizens and residents. All married couples must fil

-

•Taxes apply to United States citizens and residents. All married couples must file joint returns unless legally separated.(6) The entire tax code is indexed for inflation. Any change to the new tax code must include within the legislation the names of the legislators proposing it. The tax code can only be changed with stand-alone legislation and can only be passed with a roll-call votes.

NOTES

(1) Federal Income tax: Minimum tax of $100; All household income (all compensation) taxed at 18%, excluding only the following which are taxed at a 3% rate:

-

•Income below realistic poverty line =(3+2 if married+1 if single parent+# other dependents) x 5000; phased out with 5 or more dependents (5, 6, 7, 8+ dependents get respectively 4.8, 5.4, 5.8, 6.0 credit x $5000 in calculation of poverty line)

-

•Out-of-pocket medical expenses & medical insurance premiums exceeding: Sum of 6% of gross income plus any taxable net-worth

-

•Contribution to individual tax-free accounts (maximum is lesser of 10% of income or $10,000 per spouse)

-

(2) Net-worth tax formula: tax rate is 2% of taxable net worth. Taxable net-worth of a excludes only:

-

•$25,000 per household member

-

•Even if household owns no home, if single, the median price of a US home (now $180,000) or if married, 1.5 times that price (now $270,000)

-

•Modest education-retirement tax-free account(s) value

-

•Up to $50,000 in household and personal items and up to $5000 in small business value

-

(3) Domestic US profits = All profits x [(US sales/All sales)+(US employee compensation/All employee comp)] x .5

Business losses are not subtracted from other income and may not be carried over to another year.

Salaries of dependents and minor children of any owner with a greater than 25% ownership share may not be an

expense in determination of profits.

-

Exclusions to domestic profit distribution: Businesses with at least one full-time employee unrelated to the owner may retain up to 5% of profits in a business account for future growth. Businesses may retain an additional profits up to 15%, based on the number of additional full-time-employees (%=((FTE-1)^0.7)x2). Publicly traded corporations may retain an additional 10%. Thus, nearly all publicly-traded corporations could retain 30% of profits in corporate accounts and would be required to distribute the remaining 70% to shareholders each year. Owners or shareholders may elect to reinvest all or a portion of their distributions (for publicly-traded corporations this could be done automatically), but owners and shareholders remain responsible for income taxes on the full distribution.

-

-

(4)Excise rebate = 600 + 400 if married or with dependent - (.025 x taxable income) - taxable net-worth OR 0, whichever is larger^

-

-

(5)Cap on tax-free account value per individual (ages 17 to 70) = $8000 x (age-16) (e.g. $800,000 for a 66 year old couple).

-

Each December 30, any amount exceeding cap due to investment gain is automatically moved into linked taxable account.

-

Cap on tax-free account value per individual (over age 70) = $432,000 - (8500 x (age-70)) (e.g. $609,000 for a 85 year old couple). Tax-free withdrawal at any time for for education costs of self and immediate family members. Required tax-free minimum annual distribution of 2% of value at time of first withdrawal, which must begin after age 62 and before age 70. Spouse inherits all. Up to 50% may go into that spouse's tax-free account; however, his/her age-dependent cap may not be exceeded.

-

(6)Dependents must have income and compensation under $15,000. Dependents with less than $2000 income and compensation owe no tax and need not file a tax return.

-

^ Elimination of the payroll (Social Security-Medicare) tax is a savings for employees. However, employers pay a tax equal to the employee tax into Social Security and Medicare (7.65% of wages up to about $110,000, lower percentages for higher salaries). This would be huge windfall for businesses. Therefore, the elimination of this tax for businesses should be coupled with a mandated 38% increase in the minimum wage (from $7.25 to $10 per hour), a minimum 5% increase in salaries under $110,000, and smaller increases in salaries between $110,000 and $300,000. An increase in the minimum wage would decrease the cost to the federal government of the Earned Income Tax Credit, Food Stamps, and Housing Assistance. These savings would more than pay for the excise tax rebate for low income families, used to reduce the regressive effect of excise taxes. Currently, the federal government (other taxpayers) supplement earned incomes largely to the extent that that businesses are allowed to pay a minimum wage that falls far short of a "living wage.” Government-funded or mandated disability payments should only pay a living wage for 1) "total disability" that precludes any work more than 5 hours a week (reevaluated no less every 5 years), 2) a supplement for those capable less than 40 hours of work a week, or 3) up to two years during recovery and retraining following the disability onset.

-

Our federal tax code is over 10,000 pages. It is so complex and opaque that everyone suspects that there are special provisions that benefit the powerful and well-connected buried within it. They are right. Each year Americans spend an estimated 6 billion hours deciphering our tax code at a cost of about 200 billion dollars. Under the suggested scheme the federal tax code could be reduced to a few hundred pages. Each state’s and municipality’s tax statute could be reduced to a few sentences. Nearly all families could fill out their one-page combined federal-state-municipal tax return in less than one hour. The tax code could be easily understood, so everyone could see that all taxpayers are paying their fair share. Hundreds of thousands of tax lawyers, accountants, state revenue officials, municipal tax collectors, and toll collectors could move into more productive occupations.

The Net-worth Tax would have yielded about one-third of the revenues collected from households under the Combined Income and Net-worth Tax. These tax reforms, combined with sensible spending cuts that are two-fold larger than the total revenue increase, would yield federal budget surpluses and the elimination of the national debt over 30 years. A roughly 100% surcharge on the Federal Combined Tax would be needed to fund all state and municipal government expenditures.

Under the income-and-wealth-based tax system and rates described above, in 2007 the hypothetical working, middle-class Smiths would have had a total federal, state, and municipal tax bill of about $15,000 (rather than $28,300), and the millionaire Richs would have paid about $57,000 (rather than $32,000). The Smith's total tax bill would have amounted to 20% of their $73,000 current income and investment gain. The Richs' total tax bill would have amounted to 36% of their $157,000 current income and investment gain. The Smiths’ total tax bill is reduced from 49% to 25% of their net worth, while the millionaire Richs’ total tax bill is increased from 1.6% to 2.9% of their net worth. Seems only fair, or at least somewhat fairer.

-Peter Gloor; July 14, 2011 http://fairsharetaxes.org

CRITICAL PAGES: HOME ROMNEY TAXES SUMMARY IMAGINE! HELP US!.

SEE FULL NAVIGATION MENU AT TOP OF PAGE